What assets can I have and how much can I earn to keep Age Pension entitlement

Before I start our topic of today, first I would like to sincerely thank you for lovely birthday wishes, but even more importantly for the congratulations on reaching 1 Million views. This is an incredible achievement for this channel that I am very proud of.

So thank you for watching, thank you for your participation and for learning, so you can improve those beautiful retirement years.

Today we will continue our last week’s topic: “Age Pension improvement – empty promises” and we will continue talking about the new asset limits introduced on 1st July 2023 as well as new income limits, so how much you can earn under the Age Pension Income Test rules.

Last week I presented that table as the way to provide you with an update of value of assets under the Asset Test.

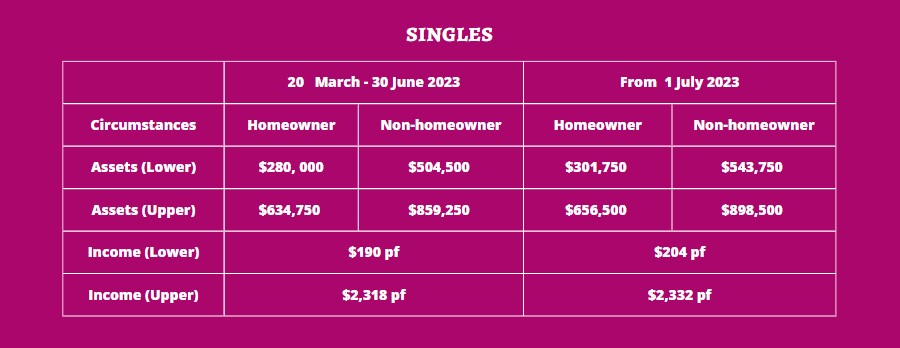

Here is the table for singles:

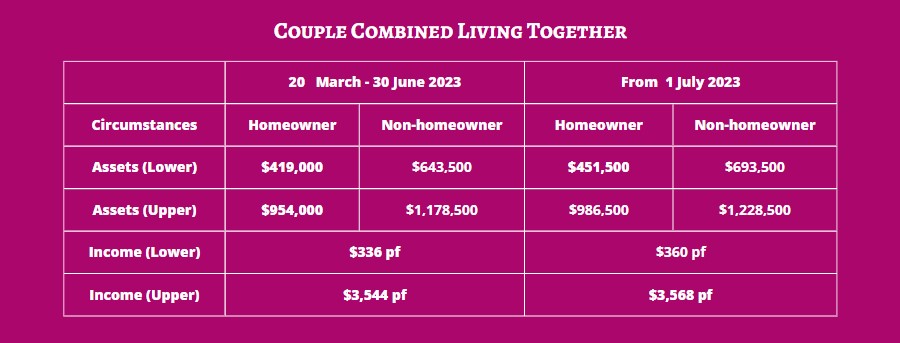

Here is the table for couples:

For singles:

- To keep the full Age Pension payment under the Income Test your income allowance has increased from $190pf up to $204pf

- The Age Pension is being cut off if your income is greater then $2,332pf, which is an increase from the previous limit of $2,318pf

For singles:

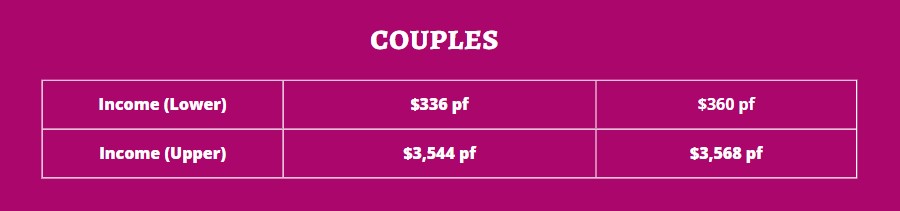

- To keep the full Age Pension payment under the Income Test, you can earn $360pf, which has increased from $336pf

- The Age Pension reduces to $0.00 when you earn more than $3,568pf, which is an increase of the previous limit of $3,544pf

Speaking about the Income Test, it appears that lots of people have a real problem understanding how this works, and in “Age Pension improvement – empty promises” I mentioned that although under the Asset Test one might be eligible for the full Age Pension based on a new Asset Test threshold, surprisingly Income Test reduces the Age Pension payment.

I agree that especially at the lower end this should not be happening. If one is eligible under the Assets test, the Income test should match it, but unfortunately often this is not the case.

So why is this happening? Let’s go over couple of case to make this topic as easy to understand as possible.

First I introduced Jane – a single woman with exactly $301,750 in assets, which is the limit to be eligible for the full Age Pension under the Asset Test.

However, based on calculations, her Age Pension is being reduced under the Income Test.

For Singles under the Income Test:

The first $60,400 is deemed at 0.25% = $151.00

The balance above of $241,350 is deemed at 2.25% = $5,430.37

The total deemed income earned for the year = $5,581.37p.a = $214.66pf

Although the new limit has been increased to $204pf, Jane’s deemed income is $214.00pf, therefore $10.66pf more than the limit. Therefore, her Age Penson will be reduced because of it by $5.33pf which is $139pf.

Let’s check Eva and Mathew from last week

They are non-homeowners with $693,500 assets that are subject to deeming under Income test.

So as we know from the last week’s video, under the Asset Test they are eligible for the full Age Pension, but I also said that under the Income Test, they will miss out on $2,120pa between them combined.

Why? Why is this happening?

For a couple:

- The first $100,200 is deemed at 0.25% = $250.50

- Balance of $539,300 is deemed at 2.25% = $13,349.25

- Total deemed income = $13,599.75 = 523.06 pf

Their deemed income is $523.06 pf, while the new limit is $360pf, therefore $163.06 pf above the limit. Therefore, their Age Pension will be reduced by $81.53pf between them, which is a reduction of the annual Age Pension by $2,120 combined between them both.

If you want the full explanation of the Income Test and how it applies to other assets and not just deemed assets, then please see: “Age Pension Income Test madness”.

But please go back to the last week’s article to fully understand the change I am talking about today: “Age Pension improvements – empty promises”.

If you are not receiving the full Age Pension, can you recognise now which of the two tests is a dominant test that reduces your Age Pension more?

If you are in this situation, there are ways to improve and maximise your Age Pension entitlement, and if this is what you would like to achieve as well as improvement of your overall level of retirement income received year after year, just book a meeting with me via my website, when we can assess if this could be achieved for you.

by: Katherine Isbrandt CFP®

Money Strategist & Retirement Planner

Principal of About Retirement