Account based pension versus annuity – which income stream is better?

At the end of March 2023, the total value of superannuation assets in Australia amounted to an incredible amount of $3.5trillion and it keeps increasing by 3.2% quarterly, which equals to $102bil 400mil.

This is an un-imaginable amount of money.

No wonder superannuation is a battlefield between all super funds trying to outdo each other in the marketing department. There is an incredible amount of fees to be earned by each super fund.

The reason I say that is for you to please always keep this in mind, super funds are a business, no matter their advertising and your job is to find the one you feel most comfortable with.

Alternatively ask for an advice from a reputable financial planner specialising in this area.

This is where you will not only be provided with a great superannuation investment portfolio specifically designed for your needs but most importantly the strategy to put all your resources together for increased income and assets longevity together with improved government support if possible and feasible.

But is it a very good idea to actually understands few concepts and not just follow blindly either advertising or advice. You still need to understand it and assess it.

One of the very first things in the subject of superannuation is your understanding of the difference between superannuation in an accumulation phase and a pension phase: “Accumulation and Pension Phase of superannuation”

Then, if you don’t know much about superannuation, there are already over 40 videos on superannuation topic on my website.

Then is the time to understand types of income streams available to you: “Account Based Pensions” and: “Annuities and your retirement”

Now, that you are equipped with the basic information let’s start our today topic:

What is the difference between account-based pension and annuity, and which one is better?

Once retired most people will need to start drawing income from their savings, and as mentioned before, superannuation most likely will be the biggest investment you have outside of your family home.

So now you will need to decide what to do with your superannuation savings and how to be provided with the best income level for your needs.

And it is not as easy as one might think, as there are many ways to skin the cat, and you need to find that one way that is just perfect for you.

And because we are all different in every possible way, your way could be completely different to the way savings are set up for you friends, neighbours or other family members.

And there are reasons such as:

- We have saved different amounts of money

- We are of different ages and of different health hence we might be expected to live for a different length of time

- We have different income or assets needs

- We want different things from our money – some want lifestyle, others want to leave a legacy

- Our understanding of financial matters could be different

- Our risk appetite can be different, some people are risk averse, others are risk takers, and then there are many others somewhere in between, but do you know where you are?

- Some are singles others in relationship

- Some people just want access to government benefits, others don’t want to have anything to do with Centrelink at all and want to remain self-funded for as long as possible.

I could continue for some time, but I think you get my point.

Therefore, now I hope you can see why every financial plan and strategy is different and why I say your retirement income streams also need to be set up for you and your needs and not what your neighbour has or tells you is the best way to go about retirement.

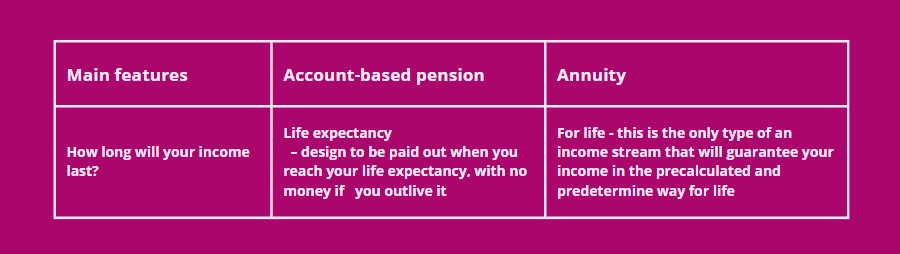

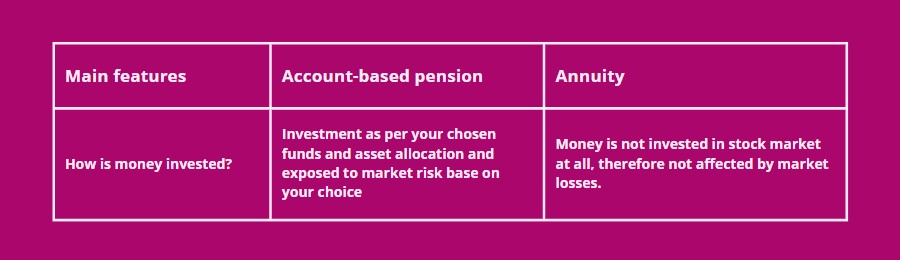

In Australia apart from Age Pension that is a form of an income stream for eligible retirees, most retirees will have some form of their own income stream and that would be either:

- Account based pension – otherwise known as an allocated pension or

- Annuity – specifically lifetime annuity

Please go back to those videos listed before if you don’t know much about those income streams.

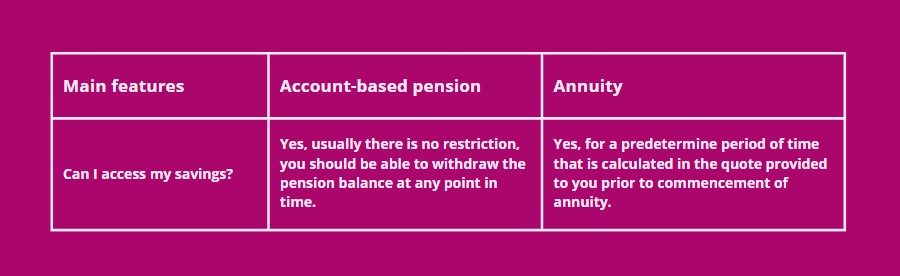

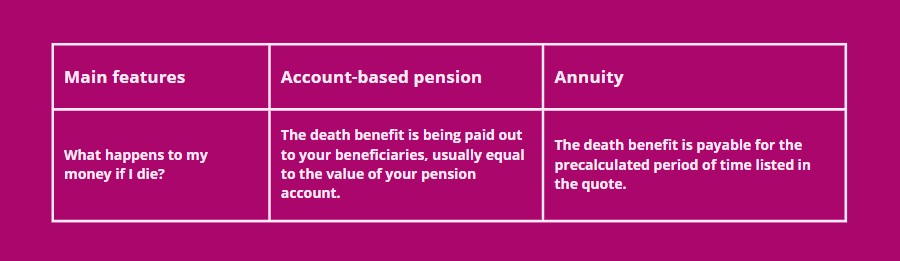

Let’s go over the main features of each income stream:

So what is the verdict? Which of those two income streams is better? Which one should you have?

The answer does not exist as each of those income streams represents different proposition that will appeal to different people for different reasons.

But what I like is to mix those income streams to have a small benefit of each, therefore, to have the best outcome I can find for my clients.

Why would I say that?

Account based pensions are great to keep your savings invested in the market and receive those exciting higher returns when the market is positive, providing that you can accept the negative years as well, as this is just simply part of the deal when investing in the market.

Annuities are boring but provide what account-based pensions don’t have – certainty, predictability, stability and security – and this is usually what most people want in retirement.

If in addition to that you know you could receive higher Age Pension payments, all of the sudden, the boring annuity is not that boring after all.

It is exciting to know that by providing yourself with a secure, pre-calculated income for life, you are also being rewarded with the higher Age Pension payment that will also continue in most cases for life.

I hope I managed to explain the difference between those two very special and very different income streams.

This is exactly what I do daily for my clients, so if structuring your income streams for the best benefit and best income set up in your retirement is what you desire, please book a meeting with me through my website AboutRetirement.com.au

By: Katherine Isbrandt CFP®

Money Strategist & Retirement Planner

Principal of About Retirement