")

The second tax haven – franking credits

Last week we were talking about: “How is tax calculated in retirement?” and the topics was investing into Australian Shares.

As I didn’t want to overload with information, I thought I would continue the subject of Australian Share investing and why I call this the second tax haven.

As you know, I always say that superannuation is pretty good for tax but investing money in retirement in a pension fund is a real tax haven. And now we are talking about the second tax haven, investing into Australian Shares.

Therefore, today we continue our discussion about investing into Australian Shares, why are they so good for tax, why retirees should pay attention to this type of investing and how the tax works depending where you purchase those shares.

Australia is one of the rare countries to have a franked dividend system in our taxation rules.

It makes our investing so very special for its tax beneficial treatment.

What that really means is that our government cannot double-dip into receiving tax from the companies we invest into, as well as from us as investors.

To make it easy to understand let’s immediately look at the example:

You made a purchase of 100 shares of CBA at the price of $100 per share. Therefore, you spend $10,000.

Now you received your dividends for the year (usually paid semi-annually) of 5%, therefore you receive a net dividend of $500.00

But when you look on your statement, you can see the explanation – franking credits $214

What that means is that CBA paid tax at the corporate tax rate of 30%, and your franking credits is let’s say a portion of that tax that was paid by CBA on your behalf for your portion of $10,000 investment, therefore on your dividends of $500

Therefore, your actual income from your $10,000 investment is a gross return of $714 for a year.

So now that you prepare you own personal tax return, depending on your marginal tax rate the following can happen:

- If your marginal tax rate is lower than company tax rate of 30%, you will receive a tax refund

- If your marginal tax rate is equal to the company tax rate of 30% there is no tax liability to pay on those dividends

- If your marginal tax rate is greater than the company tax rate of 30%, you will pay the difference of tax required.

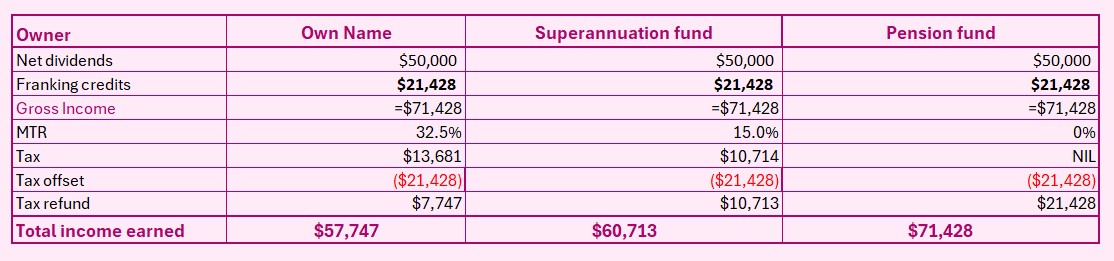

Let’s look at some examples and let’s assume that you have invested $1MIL into a portfolio of Australian Shares all paying 5% dividends 100% franked.

Therefore, your net income for the year is $50,000

Our statement indicates the level of Franking credits as $21,428

That means that your gross share income is $71,428

Let’s compare the income and tax outcome, depending who is the owner of the investment portfolio:

1. You purchased share on your own name while retired

If you bought those shares on your personal name and we assume this is your only income, tax on income is $13,681

But you have $21,428 in franking credits that you can offset again that tax bill

Therefore, after applying the tax offset, you are actually receiving a tax refund of $7,747

That sound like a very good deal to me.

But let’s now try to make it better.

2. You purchased your share portfolio within your super fund

Your super fund has to pay tax at the level of max 15%

So if the fund earned $50,000 in dividends plus $21,428 franking credits, the tax of 15% on the gross $71,428 is $10,714

Well, super fund now is eligible for the tax offset of $21,428, therefore your super is actually receiving a tax refund of $10,713

Can we still improve on that tax?

3. Now you have retired, and you moved your share portfolio into a pension fund.

So again, you received your dividend of $50,000 plus franking credits of $21,428, therefore a gross income for the pension fund of $71,428.

But look what happens now. Pension funds have $0 Tax rate, but the franking credits are refundable, therefore at the end of the financial year, your fund is eligible for the refund of the full value of franking credits of $21,428.

This is the easiest way how you can increase your income and why retirees should really pay attending to Aussie share investing.

And it is not limited to SMSF, there are number of super funds you can use for this benefit.

Just please do not buy $1Mil of one stock, your portfolio still needs to be well diversified, so speak to a financial planner to assist you with creating a well performing with tax-effective income every year.

I do hope you found this explanation a little of an eye opener. If so, and if you would like to discuss your share investing, feel free to organise a meeting with me via my website to see where you can take your investing and how you could create a very tax-effective share investing for your benefit.

By: Katherine Isbrandt CFP®

Money Strategist & Retirement Planner

Principal of About Retirement