Income required for a comfortable lifestyle in retirement

A year ago, I wrote an article “What income do I need in retirement” and many people read it, so obviously this is an important topic, and I am not surprised as we all need to know:

1. How much it would cost to live in retirement with the lifestyle we want to have

2. Are we spending more than others – we all like to compare and,

3. What is the amount of money we should have to be provided with income for lifetime?

Therefore, today I will run through a little bit of an update of this very important topic for retirement and the level of income you might need.

After all our life has changed dramatically over that last year: increase of interest rates, increase in the level of inflation, increase of living expenses – all of this has impacted on our budget and obviously now, we all need more money due to higher expenses in comparison to a year ago.

So what income do you need in retirement now, considering all those economic events and what is the magic savings lumpsum you should have according to the latest ASFA findings.

Current figures have been calculated by ASFA, which is the Association of Superannuation Funds of Australia. I have attached to this video additional information that could be of interest to you such as:

1. Detailed budget breakdowns in March 2023

2. Retirement Standard

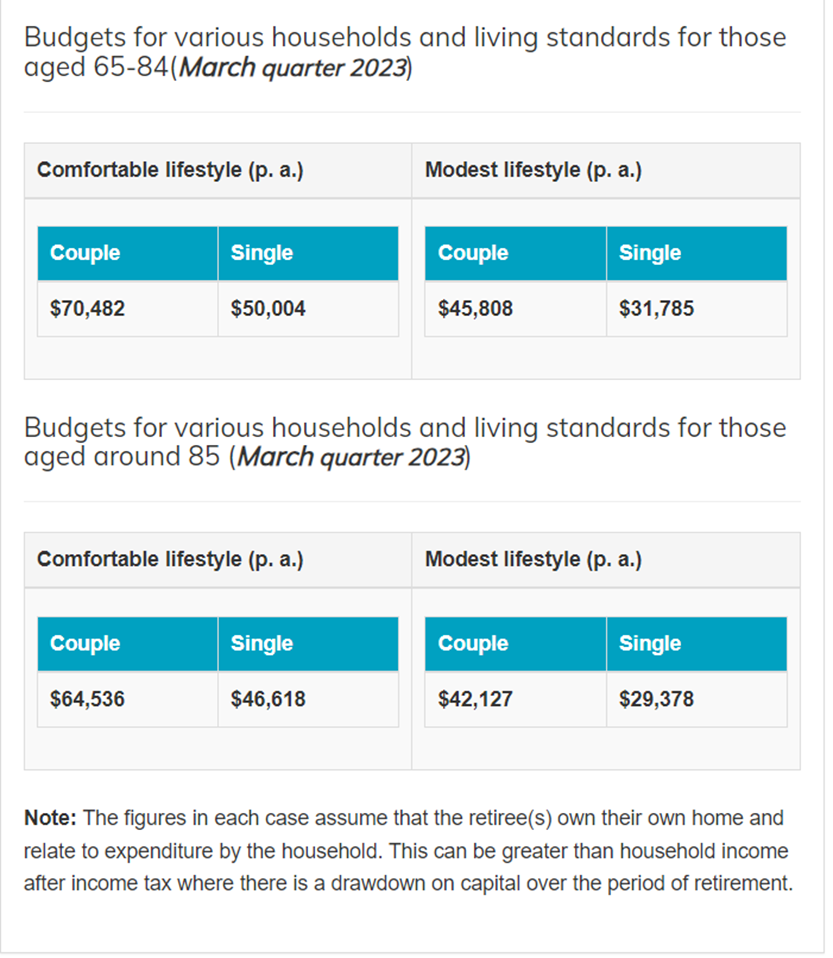

But today let’s just concentrate on this little picture:

From the table showing you can see that as a couple at age of 67 you require a lumpsum of $690,000 to have a comfortable lifestyle and as a single $595,000.

To have a modest lifestyle, all you need at age 67 is $100,000 in either case, whether you are single of a couple.

So let’s put those numbers into the test to see what income you can rely on, where the income is coming from and how long could you enjoy this lifestyle with income increase annually based on inflation.

Obviously, the outcome will be different for homeowner or non-homeowner, but somehow ASFA forgot about that little issue, as this would provide a totally different outcome for Age Pension.

Also, nothing is really listed about any other personal assets that we all have such as a car or two, home contents and just a basic cash in bank account. For many this can immediately add up to more than $50,000 in value, which again impacts Age Pension calculations, but maybe I am being too picky.

So for the sake of this exercise let’s just assume that all our cases are for home owners only, we set $10,000 car value, $5,000 home contents and just basic $20,000 in a bank account as a security savings for a rainy day.

Case 1 – Tom and Bridget both 67 years of age.

They have $345,000 saved in their respective super funds, therefore a total of $690,000 as per ASFA example, and they would like to have an income of $70,482pa subject to CPI for the rest of their lives. ASFA assumes superannuation earnings of 6%, so this is the rate I have included in my calculator for both pension accounts in retirement.

In year 1 Tom and Bridget are eligible to receive $10,186pa each from Age Pension. This is a total of $20,372pa between them. Therefore, to have an income of $70,482, they need to draw an income of $50,056 from their super funds. That is a withdrawal of 7.25% of the total balance of pension accounts, which is more than the recommended 4% minimum payment and also is more then an estimated annual return of 6%.

So most certainly you have to be prepared for the fact that your super will be reducing in value over time.

Based on my calculations, by the age of 91 they are starting to run out of money, their super funds have dropped in value substantially and can no longer support the level of income listed.

My concern however is if one of them required Aged Care placement at any point in time. The only asset left is their family home, which is a scary proposition for the partner that is of good health and wants to remain in the family home.

So as you can see you can take ASFA figures as some indication, but most certainly if you live longer than expected you will get to trouble, if you have a health issue you might have a financial issue, and there is not much of the legacy left behind.

Case 2 – Jane, single 67 years of age.

Let’s now check the same example for Jane, who has $595,000 in super and wants that income of $50,004 for life, subject to annual CPI increases:

Jane’s case is even more difficult to prove that ASFA is correct.

In year 1 she is only eligible for $2,841 of Age Pension per annum, which is only $109.30pf. That means that Jane needs to withdraw $47,163 in year 1 from her pension account to meet her target annual living expenses.

Again, by the age of 90 she virtually spend all her superannuation savings.

So as you can see, ASFA calculations is OK if you wish to be provided with that level of income for your life expectancy, but if you are lucky or unlucky to live longer, my suggestion is to plan better then the default option provided within the general calculator by ASFA.

After all this is and indicator only, and if you have a similar amount of savings as provided in those examples, those savings can be set up in the way that your income can stretch for much longer then just your life expectancy with the much higher level of Age Pension from year 1.

All you need to do is to get the full advice about your retirement income streams that is designed for you, for your needs and for your particular lifestyle and this is different for each person and for each couple.

This is why such examples are just that, just examples to make you think, question and inquire, but not to take them literally, as we all are different and have different needs.

So if you wish to have clear calculations and proper plan for your retirement, just book a meeting with me to see how I can assist you.

by: Katherine Isbrandt CFP®

Money Strategist & Retirement Planner

Principal of About Retirement